Online managers, you have to be very strong now: You didn’t invent the marketplace. The department store industry did. And, you are at risk of getting the same low margin virus as they did.

Let’s travel back in time to 1995, the beginning of our digital future. The internet protocol goes commercial, a website named Amazon sells its first book, and a Japanese toy named PlayStation makes its first Christmas appearance.

Amazon landing page in 1995 (Source:Amazon Archives)

The Birth of the Marketplace

Around the same time, the department store market, an industry light-years away from a digital mindset, begins to consolidate. The post-war retail gold rush in the US and Europe long over, out of town competition from hypermarkets and outlet centres have taken considerable market share. New category specialists and verticals emerge in urban centres and find easy ways to expand in a mushrooming shopping centre market.

A UK shopping centre as seen everywhere in the 1990s (Photo: Grimsbylive)

Whether it’s the food floors, furniture departments, white goods, or cosmetics – department stores lose market share to faster verticals or more competitive specialists category by category. To hold on to power, they take over competitors and invest outside their core markets. But rather than bring back the golden age, these attempts just shrink capital reserves.

And the more you focus on side businesses the more you weaken your DNA, i.e. making a good margin from buying and selling goods. And with under 45% of gross margin left to pay for high street rents, staff and marketing, this just further prolongs the slow death of the department store. And when you are short on margin, you are likely also short on cash flow and your shop floors have sales everywhere.

Department store in Vancouver (Photo: Brand Pilots)

And so it becomes common practice in the 1990s for brands to take over an investor role. Suppliers invest in a better shop appearance (shop-in-shop fixtures), deliver more goods with return risks (depot contracts) or sell goods at own risk with own personnel (concession stores). Eventually, brands ‘buy’ their own space, preferably near the escalator. And that’s long before Jeff Bezos discovered that paid search ranking makes for a better income than the buying and selling of goods.

And as a result of this development, department stores lose their USP and begin to look alike everywhere. With sales floors curated by Excel and KPIs, they become ever more confusing and boring for consumers. Add to this staff reductions, and department stores lose all curatorial competence. Shop floors become a wild mix of brand stores interspersed with bargain tables to grab our attention.

Are Online Marketplaces Repeating History?

Back in the early 2020s, department stores have shrunk to insignificance. Meanwhile, online marketplaces have taken over the role of one-stop convenience shopping. The Covid-19 pandemic gave online marketplaces an additional boost while brick and mortar stores were closed for months or faced with cumbersome health and safety requirements.

The world’s largest online marketplaces (Graphic: Euromonitor)

But we also see signs that the online market may approach its 1990s moment and is running out of organic growth. Is history repeating itself? Let’s look at four current trends to find out.

- Gloomy growth prospects for online marketplaces

Amazon gives a profit warning as Q4 sales may for the first time fall below the previous year. Zalando increase their marketing spending by 50% to reach the sales forecast, and the Asos CEO takes his hat. Evidence abounds that organic growth can no longer be taken for granted. But ideas and capital are still plentiful. After all, 2020-21 were the years where onliners collected billions of fresh capital to build and scale their marketplace business. And with stores dreading fresh lockdowns, there is no shortage of brands looking to go the marketplace route.

Latest media news of online marketplaces (Graphic: Brand Pilots)

- Non-organic strategies

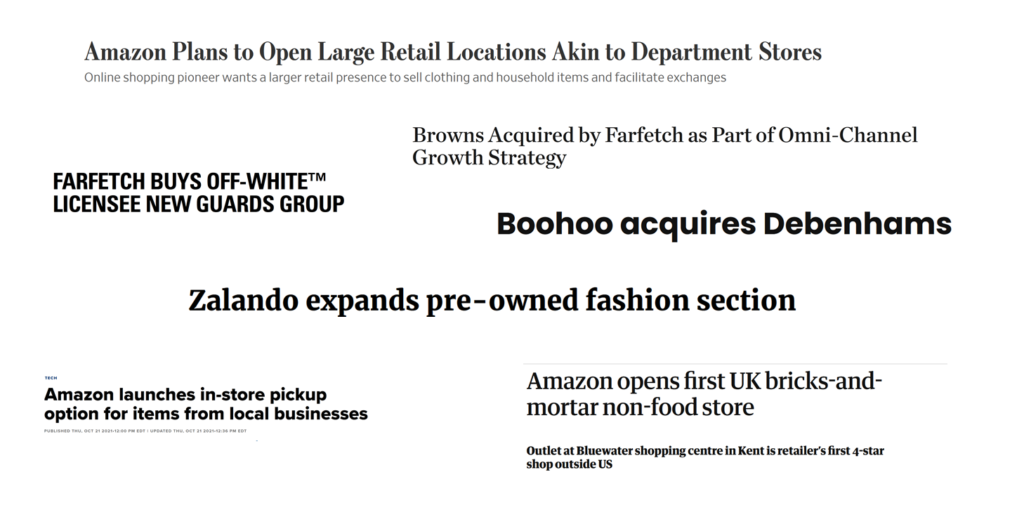

Farfetch buys retailers and brands, Boohoo acquires a dead department store, and Amazon tries the 10th retail concept. That doesn’t sound like core business or operating at scale. It has been a management reflex for decades to ‘buy’ sales when organic growth is shrinking. On the other hand, testing out new avenues and consolidating is quite literally part of the e-commerce DNA. Or do you think Jeff Bezos had any idea in 1995 that he would make 1000 x times more money from logistics and advertising than from book sales?

Market platforms invest outside their core business (Graphic: Brand Pilots)

- Crash or consolidation

With currently 400+ marketplaces, more by the month, some form of ‘natural selection’ will take place at some point. Will it be like with department stores, where only a handful of players are left in the end? That’s conceivable once the e-commerce hype is over and cheap capital hard to come by. But that may still take a few years, especially if we continue to see brick and mortar affected by pandemic waves and lockdowns.

- Low margin malaise

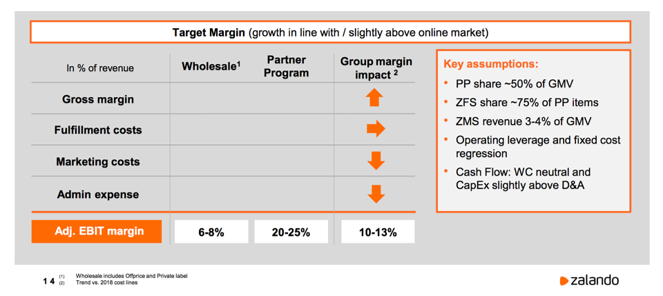

Like their urban peers, multi-brand online pure players lack gross margins. That’s not a problem for shareholders and stock markets so long as you continue to scale and grow. But when your own buying and selling isn’t getting you the margins you need, you do it the department store way and invite suppliers to operate their own store. And it pays in growth and profits for the online marketplace, as the figures Zalando shared on capital market day illustrate.

Own business at 6% EBIT and the marketplace at 25% (Zalando’s capital market presentation on the expansion of marketplace business)

Whether these four e-commerce trends lead back to a department store future for the online marketplace remains an open question. But it certainly didn’t hurt Jeff Bezos to try private labels, buy competitors and invest seven years before his marketplace was a commercial success.

And the Brand Industry?

We’ll only know what the retail world will truly look like post-Covid a few years from now. But when it comes to the online marketplace, businesses continue to invest and scale. Investment pockets are full and we are only at the beginning of a flattening growth curve that inevitably ends in a consolidation of market power.

We will see an online market that specialises and well-curated pure players earning well over 45% gross profit. In this respect, it’s best to learn how to manage online marketplaces at an early stage. This sales channel is as systemically important as department stores were in the past century, even without the pandemic. Whether you like them or not, as long as they are top convenience and occupy the number one location on mobile devices, you simply can’t do without them.

The future of brand distribution lies in smart multichannel: primarily wholesale, shop-in-shop and occasionally concessions/marketplace, stationary as well as online. In addition, social commerce in its own app, together with its own stores. If this multichannel strategy is well developed, a healthy share of the online marketplace is ideal for attracting new customers. This sales strategy beats every online pure player, both qualitatively in customer perception and in gross profits.

About the Author:

Guido Schild grew up in the industry as a consultant to brands & retailers, multichannel, multibrand, multinational. Formerly in the turnaround spin, today as a coach on the sidelines – but always looking at the strategic whole. He regularly writes about his work and the industry here.