Wholesale distribution managers knew it all along, traditional brand wholesale wouldn’t last forever. And 2020 saw an acceleration of change that began long before the pandemic: the termination of mediocre businesses.

But turmoil in wholesale distribution isn’t over yet; ahead lie at least one to two more years of trouble and possibly major strategy changes at online pure players.

This update from our ongoing executive dialogues on the Future in Brand Distribution will outline why:

- Next years’ sales are a Fata Morgana

- Brand wholesale distribution will remain a cash cow for years to come

- Winners and losers may be different than you think

- Department store strategies are a benchmark for online pure players

- Brand wholesale organisations need to prepare for what’s coming

Adidas’ strong commitment for D2C will not change that wholesale distribution will still be its largest channel in 2025 (Photo: Adidas, NY Flagship)

Next Years’ Sales Are a Fata Morgana

Lets face it, Covid-19 hit brand wholesale distribution hard. And unlike in D2C (direct to consumer), not much could be done to improve the situation. Some of the biggest retail customers went bankrupt, and with them went the receivables. The uncertainty extends to retailers that survived on their reserves, as they may not have much left for coming years. And who knows how much more pressure credit insurers and banks will put on the offline retail market.

It’s safe to assume that monthly sales reports for the next 2-3 years may be a Fata Morgana until the cash for delivered goods is secured. Developing a strong understanding of the new realities in wholesale distribution, online and offline is essential. But even more importantly, understand your customers’ business model and what it means for their finance and future.

‘To be or not to be?’, Ludwig Beck, a past-time retail destination and important brand account. Like for many, only the future will tell its importance as local hero (Photo: brand pilots)

B2B Brand Distribution Will Remain a Cash Cow for Years to Come

Brand managers will agree that 2020 online sales growth creates hope for the future. But it remains wholesale distribution (retail and online) that pays the bill for most D2C investments.

Yes, collecting cash from retail customers is a challenge, but it still finances the largest portion of overall brand costs. That makes it very valid to preserve and nurture wholesale distribution. In fact, it even holds many more growth opportunities. As wonderful as D2C sales are, in terms of brand control, own retail or e.shops are capital intensive businesses and for most of the year cash flow negative. Additionally, they are still not (and may never be) as profitable as wholesale.

Prada, an e.shop latecomer now committed to D2C also online (Source: Screenshot Prada)

That, among other reasons, is probably why no digital native lifestyle brand has yet passed the $ 100m revenue threshold without starting wholesale distribution. Brand B2B distribution is what is famously called a ‘cash cow’. That is, “products or services that consistently generate substantial revenues that can be used to invest in markets that offer higher growth rates.”

In other words, D2C managers should be very grateful for the contribution of their wholesale colleagues. And brand wholesale distribution may prevail, especially with the help of booming online pure players. Having financially strong multi-brand retail customers, partner retailers or online pure players in the sales portfolio enables future investments in more D2C. Long live the cash cow!

If you’re as strong as Nike you can be very selective about your wholesale distribution partners (Photo: brand pilots)

Winners and Losers May Be Different than You Think

Most brands report wholesale by region or country, and by online customers vs. brick & mortar (which can be misleading, as brick & mortar key accounts sell ~50% online). Meanwhile, the strategically more relevant reporting is ‘merchant’ sales vs. ‘letting’ sales.

A short trip down last-century department store memory lane exemplifies why. Around the 1990s, the department store market saw a split into basically two business models. The first model were retailers that bought and sold products with a decent margin, the traditional role of a retail merchant.

Global multibrand retailing made in France, not everybodies’ wholesale account, but a business model with long-term perspective (Photo: Decathlon Berlin)

The second model were department stores that gave up floors, shops or categories and built their success on concession stores, by letting space to brands and retailers. That could for example mean the top floor is left to an electronics chain or parts of the ground floor to luxury brands, Starbucks or even H&M. The final stage arrived when the beauty department was given away entirely, for example to Sephora.

While the ‘merchant way’ preserved the department stores’ own identity, it carried the economic risk of keeping inventory and selling products. It’s a capital-heavy strategy, needed regular investments in remodelling stores and technology, not to mention the (pre)financing of stock.

‘Letting’ or concession retail, on the other hand, was light in capital. Brands were investing and carried the inventory risk while paying the department store a fixed commission. Most department stores that went the ‘concession way’ big time lost their identity in the process, and it didn’t stop them from dying. Letting does not turn an unsuccessful merchant into a successful shopping centre.

Galeria Karstadt Kaufhof, one of many department store chains where a move towards more concessions did not prevent bankruptcy (Photo: Berlin Alexander Platz, Wikipedia)

Department Store Strategies Are a Benchmark for Online Pure Players

Back to 2021, we observe that online pure players are replicating department stores’ strategy with their marketplace route: Own business is not returning enough to generate attractive profits, so they let space to third parties and call it a marketplace. Ok, that is not completely how the online pureplayer explain their strategy, but the underlying business logic is the same.

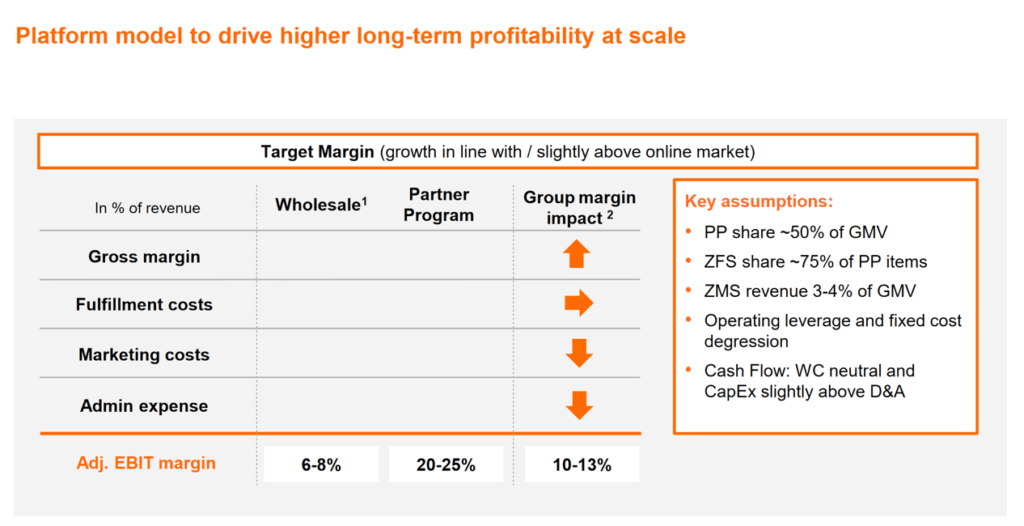

Onliners are not very transparent about true strategies, but from time to time IPO filings or investor information tell a story. Zalando, for example, gave some hints in the 2020 autumn roadshow documents.

Zalando marketplace revenues are expected to be four times more profitable than Zalando’s own business (Graphic: Zalando)

With that difference in performance it isn’t a surprise that the market place gets a lot of Zalando’s marketing budget.

And the lack of profitability in own business is by no means a Zalando exclusive. Exiting Commerce, my favourite source for understanding the online market, regularly does a very good job at showing similar developments at Amazon and other online pure player. Profits from own trading, the core of the online pure player business, stay rather low. That is forces onliners to work on strategies to extend their services to third parties.

For brands that means:

- If the pureplayer’s profit gaps continue what does this mean longterm to your wholesale with them?

- If online pros (like Zalando) only earn 6-8% EBIT from buying and selling, what qualifies brands to do it more successfully on the market place?

To me it says, brands investing blindly building marketplace business can quickly experience the same as they did in department store retailing: They realised late that they went wrong, and when they did, the channel was too large to drop it. Be smarter this time, control the growth from the beginning.

It’s certainly too early to predict that online players will go the same fate as department stores. But allow me to place a big strategic question mark with you – In any case, stay alerted of the vulnerability of our new B2B wholesale distribution.

Amazon is not the sexiest online place for lifestyle brands. Still, for many too important to skip (Source: Screenshot Amazon March 2021)

From Cinderella to Princess: Brand B2B Distribution Needs a Revamp

If your brand’s sales mix is like most, wholesale distribution deserves all your attention now. Do you sell to a highly energetic, fast-changing market by the means of 2019 wholesale structures? It’s time to wake up and make changes for what’s to come.

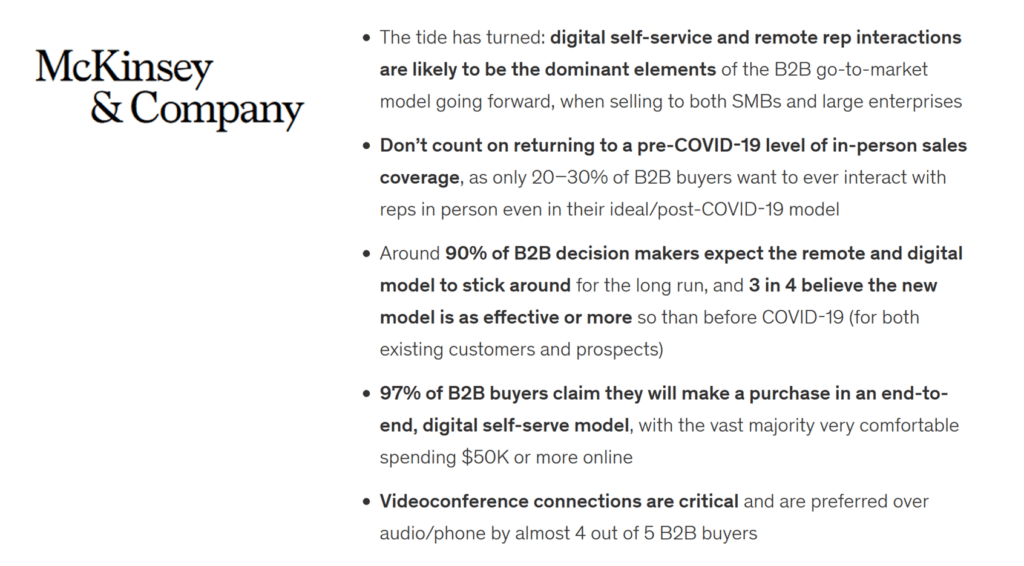

Strong bullets from the global strategy authority on changes in b2b and retail (source: McKinsey, Global B2B decision-maker response to COVID-19 crisis)

How much have you invested to advance your most important distribution channel over the last 10 years? To understand how the wholesale business and its processes have changed (long before Covid-19), ask yourself these questions:

- Are sales risk assessment tools up to date for the market changes to come?

- Selling on marketplaces differs from selling wholesale online like concession retail differs from wholesale. You knew that and therefore had your retail team taking care of concession, is your e.shop team managing market places or your wholesale team?

- Who in the online market is only pumped up with investors capital, and who has a business model worth growing with long-term?

- Offline product launches with key accounts were season kick-off highlight, and are a thing of the past. What instead will create a unique brand experiences with collection launch?

- Traditional trade shows likely are gone forever. How do you reach and nurture small accounts next season?

- When selling wholesale online, do you invest in own systems? Or, which B2B platform can you trust longterm?

If you don’t have all the answers yet, there is still time to revise strategy and organisation, structure and tools, and harvest in a fast-changing market.

Because, whether you consider wholesale sexy or not, it will remain the financial backbone for many more years to come. And as long as your total D2C isn’t clearly above 50%, wholesale remains your most important distribution channel. Invest in it, to operate it professionally. To be well-prepared for the next pandemic to come.

About the Author:

Guido is a brand strategy advisor deeply ingrained with the belief that all distribution channels have to be healthy, and growth needs to be well-balanced. To argue with him about wholesale brand distribution or ask for his advice, get in touch with him via LinkedIn.